One Lender Grew for 20 Quarters Straight. The Engine? Secured Finance.

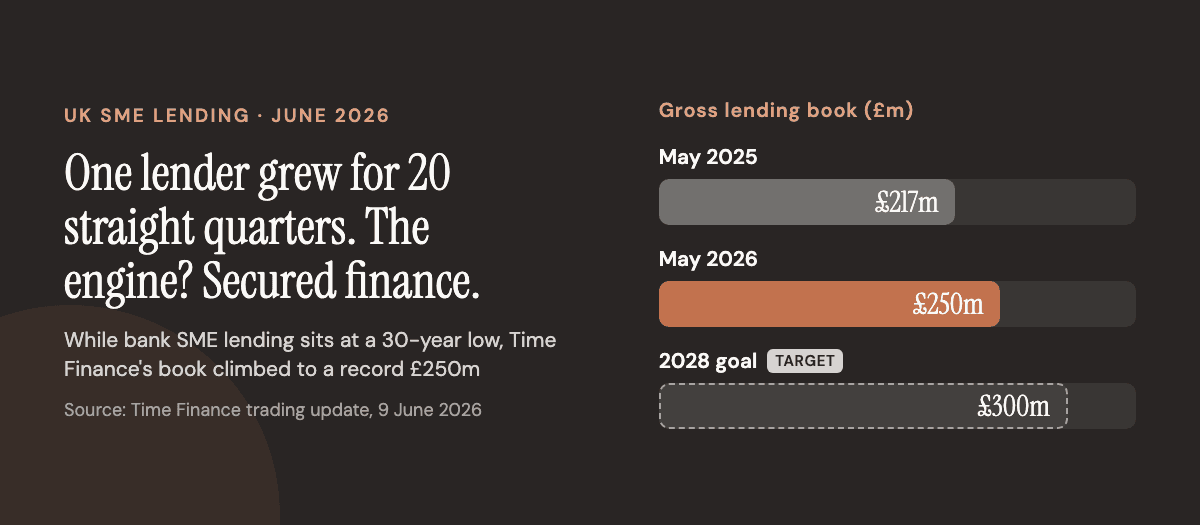

Every story we've written this year says the same thing: UK bank lending to small businesses is at a 30-year low, high street rejection rates have tripled since 2018, and the big four have walked out of invoice factoring entirely. So here's a number that cuts the other way. On 9 June, the Bath-based lender Time Finance reported that its gross lending book had passed £250 million for the first time, up from £217m a year earlier. It was the company's 20th consecutive quarter of growth. Five years. Not a single quarter in reverse.

That run spans a pandemic, the fastest rate-hiking cycle in a generation, and an SME credit squeeze that has dominated the headlines. So the interesting question isn't whether this lender grew. It's how, and the answer says something useful about where SME money is actually flowing.

The headline: a record book, and a clear target

The bare facts, from Time Finance's 9 June trading announcement:

- Gross lending book: £250m at 31 May 2026, an all-time high, up roughly 15% from £217m a year earlier

- 20 consecutive quarters of growth, every quarter since 2021

- A stated strategic target of a £300m+ book by May 2028

A full-year trading update is due on 25 June, with audited results in September. But the milestone itself is the story, because it lands precisely while the consensus says SME finance is broken. It isn't broken: it has moved. And it has moved toward a particular kind of lending.

The real story: it's not cash, it's collateral

Here's the part the headline number hides. Time Finance is not growing by writing unsecured cheques. It is growing by lending against things.

In its most recent interim results (the nine months to 28 February 2026), the company spelled it out: invoice finance and hard asset finance now make up 96% of all new lending and 88% of the overall book. Own-book origination, the loans it funds off its own balance sheet rather than broking on, rose 27% to £86.5m. Revenue was up to £28.3m and pre-tax profit to £6.2m, lifting the margin to 22%.

Read that back. The fastest-growing part of this lender's business is the part backed by a tangible asset: a piece of machinery, a fleet of vehicles, or a book of unpaid invoices. The deliberate shift away from unsecured, toward secured, is the reason the growth has been so steady. When your lending is collateralised, your losses are lower and your appetite is more durable through a downturn. That's not a quirk of one AIM-listed lender. It's the logic the whole specialist market is running on.

Why secured finance is where the resilience is

Strip away the company-specific detail and you're left with a signal for any business owner trying to raise money in 2026.

The capital that has pulled back hardest is unsecured, relationship-based bank lending: the overdraft, the unsecured term loan, the facility your bank manager used to wave through. That's expensive for banks to hold against their capital, and it's the first thing they ration when they get cautious. It's why high-street rejection rates have climbed so steeply.

The capital that has held up, and in places grown, is lending tied to an asset:

- Asset finance against equipment, vehicles, plant and machinery. The lender owns or has a charge over the kit, so the risk is contained. This is the bigger of Time Finance's two engines, and the British Business Bank recently backed a £700m asset-finance programme precisely because it's seen as a reliable way to get money into established businesses.

- Invoice finance against your debtor book. You release cash tied up in unpaid invoices instead of waiting 30, 60 or 90 days. It's the route the big four banks abandoned, which is exactly why independents like Time Finance, Bibby and Novuna have been able to grow into the space they vacated.

The distinction matters because it changes the question you should be asking. It isn't "will a lender give me money?". In the abstract, the answer is increasingly no. It's "what do I have that a lender can secure against?" If the answer is equipment, a fleet, or a healthy invoice book, the market is far more open to you than the rejection statistics suggest. Our guide on secured versus unsecured business loans walks through how lenders actually weigh the two.

What this means if your bank just said no

Three practical takeaways:

- A high-street "no" is a comment on the product, not your business. Banks are rationing unsecured cash because it's expensive for them to hold, not because your company is unfundable. The same business that gets declined for an unsecured overdraft can often be approved in days for finance secured against its own assets.

- Match the finance to what you own. Equipment-heavy? Asset finance. Sitting on a pile of unpaid invoices? Invoice finance. Asset-light but still need working capital? That's where the unsecured market and specialist lenders come in: see how to get an unsecured business loan in the UK for what those lenders look for.

- The lender growing 20 quarters straight is one you've probably never banked with. Time Finance, like most of the specialists filling this gap, isn't on the high street. The capital is out there, but reaching it means knowing which of the dozens of asset and invoice finance lenders fits your situation, and approaching them in the right order.

The grim reading of 2026 is that bank lending to small businesses has collapsed. The more useful reading is that a different kind of lending, patient, collateralised, and run by people who've spent decades doing it, has quietly been growing the whole time. A lender that has grown every single quarter for five years isn't an anomaly. It's a map of where the money went.

If your bank has said no, or you simply want to know what the wider asset and invoice finance market would offer your business, we'll search it for you. The right lender is probably out there: it's just not the one you've always used.

Further reading: the scale of that quiet growth is now official. The FLA's first Impact Report calls asset finance the hidden engine behind UK growth, with £69bn of new lending in the first five months of 2026. And with access speed now as decisive as price, new Shawbrook research finds 1 in 5 firms lost a deal waiting for finance.