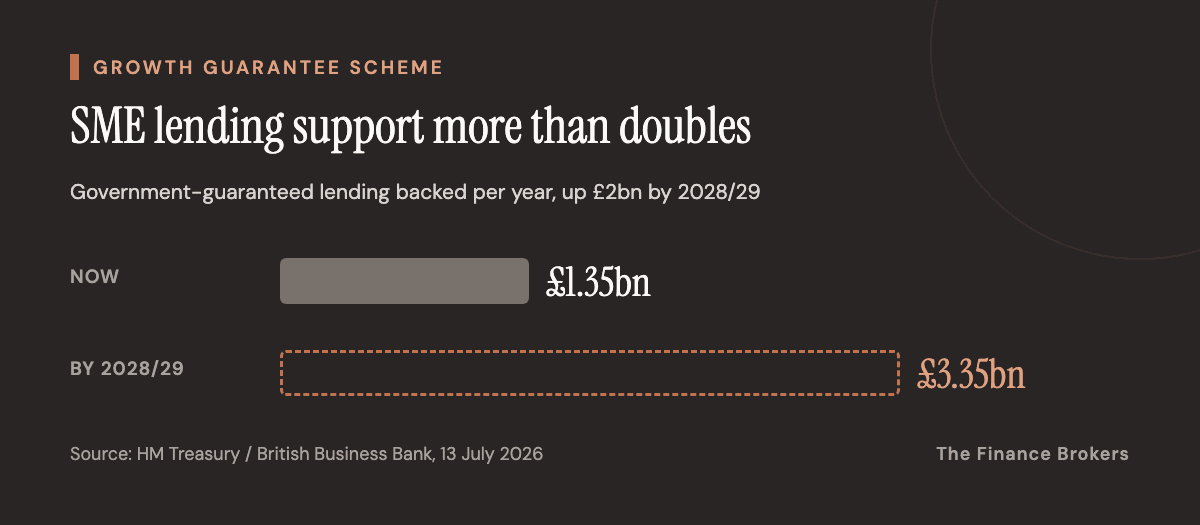

The government just made its biggest move on small business lending in years. Ahead of the Chancellor's Mansion House speech, the Treasury confirmed that the Growth Guarantee Scheme will be expanded to support an extra £2bn of SME lending a year by 2028/29. That more than doubles the total it backs, from £1.35bn to £3.35bn annually.

And the changes go further than the headline number. Loan terms are getting longer, the eligibility net is getting wider, and thousands more businesses are meant to qualify. For any SME that has heard "no" from a lender lately, this is worth understanding properly.

What actually changed

Three things moved, and each one matters on its own.

The scheme doubled in size. Supported lending rises from £1.35bn to £3.35bn a year, an extra £2bn of capacity by 2028/29. The British Business Bank, which administers the scheme, estimates it will support around 20,000 businesses a year, up from 8,000 today. That is a 150% increase in reach.

Terms got longer. The maximum loan term is extending from six to 10 years for facilities up to £1.1m. If you have been putting off a bigger investment because the repayments only worked over a decade, not six years, that maths just changed.

Eligibility widened. The turnover ceiling rises from £45m to £54m. A band of larger, established SMEs that were previously shut out of the scheme are now inside it.

The guarantee itself stays the same: the government covers 70% of the lender's exposure, on facilities up to £2m. According to the Treasury, every £1 committed to the scheme supports roughly £10 of bank lending, and it has already channelled £3.7bn to smaller firms, £2.5bn of it outside London and the South East.

Why this is a bigger deal than it looks

The Treasury puts the gap between what SMEs want to borrow and what they can actually access at between £1.6bn and £4.1bn a year. That gap is the whole problem. Viable businesses with real orders and real growth plans still get turned down, not because they are bad risks, but because the lender cannot get comfortable with the downside.

That is exactly what a guarantee fixes. When the state absorbs 70% of the loss on a default, a lender that would otherwise decline a thin file can say yes. The Chancellor, Rachel Reeves, framed it plainly: small businesses "for too long have heard 'no' when trying to raise funds." Business Secretary Peter Kyle added that "access to finance should never be the barrier between a good idea becoming a great British business."

The term extension is the quiet winner here. A 10-year horizon changes what you can sensibly borrow for. Fit-outs, plant, a second site, a machine that pays back over eight years rather than four: all of these become financeable when the repayment schedule can stretch. Six years forced a lot of good projects into a shape that did not work.

The catch nobody mentions

Here is the part that gets lost in the announcement. The Growth Guarantee Scheme is not a lender, and it is not free money. It is a guarantee that sits behind an ordinary commercial loan. You still borrow from a bank or a specialist lender, on their rates, and you are still fully liable to repay in the normal way. The guarantee protects the lender, not you.

So the scheme does not remove the two things that actually decide whether you get funded: whether your business stacks up, and whether you are talking to the right lender for your situation. It de-risks the lender's decision on a viable-but-marginal file. It does nothing for a deal that is with the wrong lender in the first place.

That distinction matters because the scheme runs through more than 50 accredited lenders, and not all of them offer every product. It is not a single door you knock on. It backs a spread of facilities, from term loans and overdrafts to asset finance, invoice finance and asset-based lending. Which lender, and which product, is the whole game.

The lenders are already lining up

What is telling about this announcement is who welcomed it. The endorsements ran from the high-street giants (NatWest, Lloyds, Barclays, Santander, HSBC) through to JPMorganChase and, notably, Allica Bank, the challenger built specifically for established SMEs.

That mix is the point. The scheme is not just topping up the banks that already dominate SME lending. It is fuel for the specialist and challenger lenders that have been taking share precisely because they say yes where the high street says no. A bigger guarantee pool, longer terms and a wider eligibility band all play to their strengths. We have written before about where SME funding is actually going, and this pushes further in the same direction.

For a borrower, that is good news and a navigation problem at the same time. More lenders competing for guarantee-backed deals means more choice and, usually, sharper pricing. But it also means the "right" answer for your business could sit with a name you have never heard of, offering a product you did not know applied to you.

What to do with this

If you have been sitting on a growth plan because the funding felt out of reach, the ground has shifted in your favour. Longer terms, a wider net, and a much larger pool of guarantee-backed lending are all now in play, and the lenders best placed to use them are the ones most likely to fund a real, viable business.

The scheme rewards borrowers who come to it correctly matched: the right product, the right lender, a file presented the way that lender needs to see it. That is where a whole-of-market broker earns its place, and it is exactly the work we do every day, whether the answer is an unsecured business loan, asset finance for equipment and vehicles, or a facility secured against what the business owns. If you are weighing up how to fund the next step, it is worth understanding the difference first.

If you want to know which lenders are best placed for your situation under the expanded scheme, get in touch. It costs nothing to find out where the yes is.