For the better part of a year, every headline about short-term property finance said the same thing: record books, record completions, a sector going mainstream. The figures the Bridging & Development Lenders Association (BDLA) published yesterday say something different. Bridging completions fell 28% in the first quarter of 2026, to £1.8bn. Development lending fell harder, down 34%.

After a run of "specialist lending is unstoppable" stories, including a few we've written ourselves, that's a number worth sitting with. But the moment you look past the headline, the story isn't a market in retreat. It's a market that's grown up.

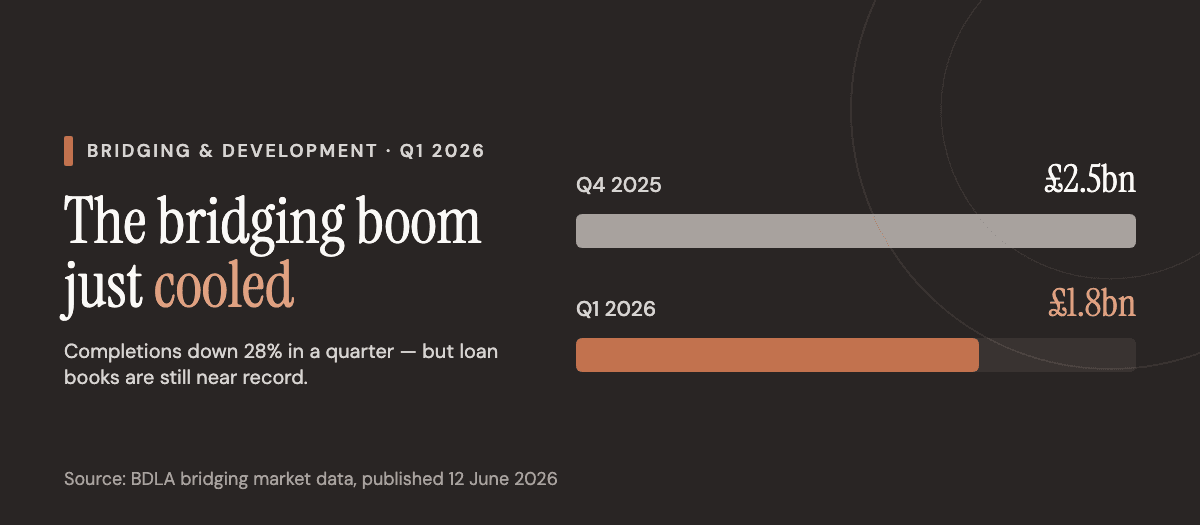

What the BDLA actually reported

The Q1 2026 numbers, measured across the association's member lenders, are unambiguous in direction:

- Completions: £1.8bn, down from £2.5bn in Q4 2025, a 28% fall

- Applications: £9.9bn, down from £11.7bn, a 15% fall

- Development lending: £276.5m, down from £420.3m, a 34% fall

- Second-charge lending: £131.3m, down from £145.8m, a 10% fall

- Average loan-to-value: 56.64%, down from 58.64%

So volumes are down across the board, and developers pulled back hardest. That's the part that should give a property professional pause: development finance, the capital that turns sites into stock, contracted by a third in a single quarter.

Adam Tyler, the BDLA's chief executive, framed it plainly: "After a sustained period of strong growth, it is not surprising to see the market move into a more measured phase." He attributed the cooling to "wider economic and geopolitical uncertainty": the same uncertainty around rates, property values and transaction volumes that's slowed the whole market, not just the short-term end of it.

One quarter, two datasets, and they don't actually disagree

Here's where it gets interesting. A few weeks before the BDLA release, Bridging Trends, the long-running index compiled from a panel of specialist brokers and lenders, reported its own Q1 2026 read. Its verdict? The market "holds steady." Total lending of £199.2m, an average rate of 0.82% a month, average LTV down to 52%, and investment-property purchases the single most popular use of a bridge.

So one report says lending fell off a cliff and the other says it held firm. Which is right?

Both. They're measuring different things, and the reconciliation is the whole point. The BDLA aggregates the value of completions across its full lender membership, so it swings with big-ticket and development deals. Bridging Trends tracks a broker panel's transaction flow, which skews toward investment and buy-to-let purchases and moves far more smoothly. We made the same point a fortnight ago about SME lending data, that a structural measure and a flow measure can both be true at once. Same lesson here.

Strip away the methodology and both datasets point in one direction: a more selective, lower-leverage, purchase-led market. Average LTVs fell on both measures. Investment purchases held up while heavier, riskier use cases (major refurbishment, business-purpose borrowing) thinned out. As Sonny Gosai of Brilliant Solutions put it, the quarter showed "a bridging finance market that remains resilient and increasingly selective."

Why this isn't a credit crunch

A 28% drop in completions sounds like lenders slamming the door. The underlying data says the opposite.

The money is still there. Total lender loan books stood at £11.5bn at the end of March, within touching distance of the record £13bn-plus the sector reached at its 2025 peak. Capital isn't leaving the asset class; it's being deployed more carefully. As we covered last week, global banks are still pouring wholesale funding into UK specialist lenders: the plumbing behind these loan books is, if anything, deeper than ever. Since then that capital has gone a step further, buying a specialist lender outright rather than just funding one.

Falling LTVs are a sign of discipline, not distress. When average leverage drops from 58.6% to 56.6% in a quarter, that's lenders pricing risk sensibly into a more uncertain market, not refusing to lend. Chris Oatway, founder and chief executive of brokerage LDN Finance, made the point in the Bridging Trends data: "Investor confidence remains strong, but the standout trend is the reduction in average LTVs." Confidence, with discipline.

Lower volumes mean more competition per deal. This is the part that gets missed. When the number of transactions falls but the capital available doesn't, lenders compete harder for the deals that do come through. Raphael Benggio, director of bridging at MT Finance, noted that "investors and landlords in particular seemed to be maximising bridging's potential" in the quarter: the experienced, well-prepared borrowers leaned in while others waited. The pull-back was in demand and caution, not in lender appetite.

What it means if you're raising finance now

A quieter market is, counterintuitively, often a better one to borrow into, if your case is well put together.

- Well-presented deals win on terms. With lenders competing for fewer transactions, a clean application (credible exit strategy, realistic valuation, evidenced experience) has more pricing leverage than it did at the top of the cycle. Rates from the prime end of the market are still sharp.

- Lower leverage is the new normal: plan for it. If you modelled a project on 70%+ day-one leverage, the Q1 numbers are your warning to stress-test at a lower LTV. That changes how much equity you bring and how you stage the raise. Our guide to how development finance works walks through the gearing maths, and development finance rates sets realistic expectations.

- Whole-of-market matters more when the market is selective. When every lender is tightening at a slightly different pace, the gap between the best and worst terms widens. The right bridging finance or development finance facility for your scheme is harder to find on your own, and more valuable when you do.

The development-lending drop is the figure to watch over the rest of 2026. A 34% quarterly fall is real, and if it persists it tightens the pipeline of new housing stock. But on the evidence we have (near-record loan books, disciplined LTVs, lenders still funded and still competing) this reads as a sector catching its breath after a record run, not one shutting up shop.

The pipeline question has since sharpened: England missed its housing target by 91,400 homes, and a good share of that gap sits on consented sites that are simply unfunded.

If you're weighing a bridge, a development facility, or a refinance of an existing short-term loan, the door is more open than a 28% headline suggests. The difference now is that it opens for the deals that are properly structured. Talk to us and we'll tell you honestly where your scheme sits.