Funding 365 Just Sold to a Global Fund. The Bridging Shakeout Is Real.

A global investment firm has just bought one of Britain's established bridging lenders outright. Not a funding line. Not a minority stake. The whole platform, the existing loan book, and every new loan it writes from here.

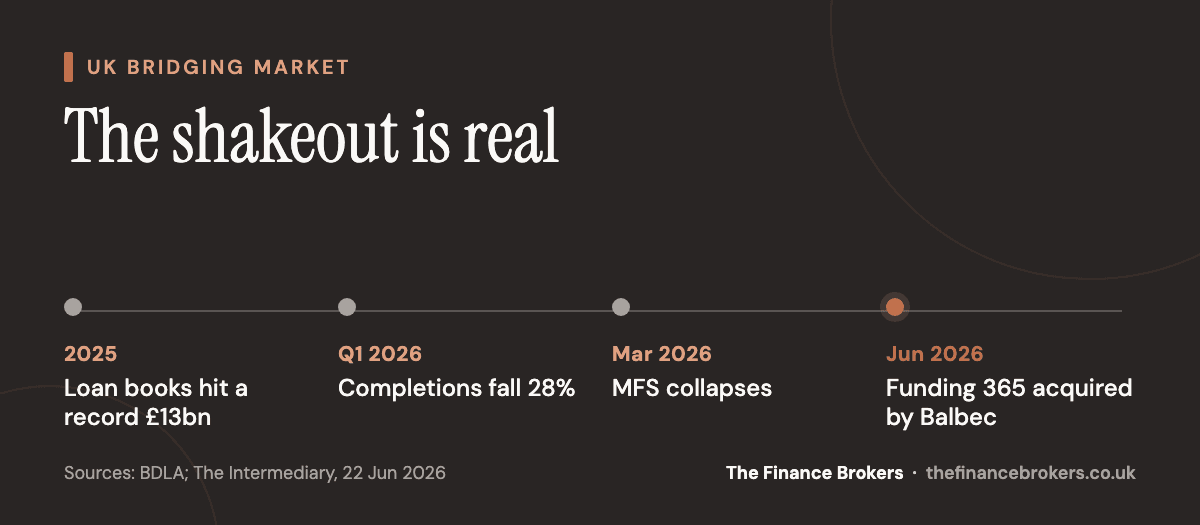

On 22 June, US alternative-investment manager Balbec Capital acquired Funding 365, a specialist property lender that has been a recognised name in UK bridging since 2013 and has written more than 1,700 loans. It is the clearest signal yet that the UK short-term lending market has moved into a new phase. The record-breaking boom is over, and the consolidation has begun.

What actually happened

Funding 365 was founded in 2013 by a team out of Goldman Sachs and Barclays Capital, and built a reputation for fast, first-charge bridging, development and specialist buy-to-let lending. Balbec Capital is a global firm that specialises in asset-based credit and real estate, deploying capital on behalf of institutional investment funds.

The terms were not disclosed, but the structure of the deal is the interesting part. Balbec acquired the origination platform, the existing portfolio, and the newly originated loans. Managing director and co-founder Michael Strange and director Paul Weitzkorn stay on to run the business day to day, and existing borrower and broker relationships continue unchanged.

"Joining forces with Balbec marks an exciting new chapter for Funding 365," Strange said. The Balbec relationship, he added, will let the lender "develop new products, grow our origination volumes, and serve our broker partners and borrowers even more effectively." From the buyer's side, Ryan Singer, Balbec's partner and head of residential credit, was blunt about the rationale: "Owning an origination and servicing platform is essential to effectively access the UK specialist lending market at scale."

Read that last line again. A global fund has decided the way to get money into UK property is not to lend to a British originator. It is to own one.

This is not one deal. It's a pattern.

We have spent the last few months documenting the same market from three different angles, and the Funding 365 sale is the thread that ties them together.

Start with the boom. The Bridging and Development Lenders Association reported sector loan books surpassing £13bn in 2025, with completions up 42% year on year. Bridging had gone mainstream.

Then the cooldown. In June we covered the 28% fall in bridging completions in Q1 2026, with development lending down even harder at 34%. That was not a credit crunch. Loan books stayed near record levels and average loan-to-values fell, which we read as discipline rather than distress: a sector catching its breath after a record run.

Then the casualty. In April, we wrote about the collapse of Market Financial Solutions, a bridging lender that had posted £71.6m of turnover and grown profits 163% before administrators arrived to a claimed £1.3bn shortfall. The lasting effect, we argued at the time, would be tighter due diligence from institutional funders and governance becoming table stakes rather than a differentiator.

And now the consolidation. A well-run, well-regarded lender has been bought by a global fund that wants to deploy capital into UK property at scale and has concluded the smartest way to do it is to own the machine that originates the loans. Put the four together and the shape is obvious. The weak get weeded out. The strong get bought. The market that emerges is fewer, larger, better-capitalised platforms.

Why ownership is a bigger signal than a funding line

A fortnight ago we wrote about global banks pouring wholesale funding into UK specialist lenders: JPMorgan backing Roma Finance, Deutsche Bank renewing a £200m line with Funding Circle. That was institutional capital renting space on someone else's balance sheet. A funding line can be drawn down, repriced, or pulled.

An acquisition is a different order of commitment. When a global fund buys the platform outright, it is taking on the brand, the underwriting team, the technology and the regulatory permissions, and betting that owning the originator beats funding one. Balbec said as much. That is capital putting down roots, not passing through.

For a market that spent 2025 worrying about where the money would come from, that is a reassuring answer. The capital backing UK bridging is not leaving. It is changing from a tenant into a landlord.

What it means if you borrow on bridging finance

For most developers and investors, consolidation is good news with a catch.

The good news: deeper pockets and more products. A lender backed by an institutional owner can fund larger loans, hold them for longer, and build out new products without scrambling for a funding line every quarter. Strange's own stated ambition, to grow origination volumes and widen the product range, is exactly what borrowers benefit from. Expect the surviving platforms to compete harder on terms, not retreat.

The catch: who owns your lender now matters as much as the rate. This is the same lesson the MFS collapse taught, only from the opposite direction. When the market is consolidating, the question is no longer just "what is the rate" but "who stands behind this lender, how stable is their funding, and will they still be writing loans when I come to refinance." A mid-deal change of ownership, or worse a collapse, is the single biggest avoidable risk in short-term finance, because your exit strategy depends on a lender that is still there to complete.

That is where a whole-of-market broker earns its place. We watch which lenders are well-funded, which have just changed hands, which are tightening quietly and which are leaning in. We know the difference between a lender with stable institutional backing and one running on a stretched funding line. When you are weighing a bridge or a development facility, knowing what good bridging finance criteria look like and which lenders genuinely meet them is the difference between a deal that completes and one that stalls.

The UK bridging market is not shrinking. It is growing up. The Funding 365 sale tells you the capital is committed and the strong players are getting stronger. The job now is making sure your next deal lands with one of them.

Thinking about a bridge, a development facility, or a refinance of an existing short-term loan? Talk to The Finance Brokers. We place deals across 300+ lenders, and we vet every one of them on your behalf.